Investing Doesn't Have to Be Complicated. Here's Where to Start.

Key takeaways

- Investing doesn't require a lot of money or experience – it only requires a starting point.

- The earlier you start, the more time your money has to grow.

- Understanding your risk tolerance and your options makes the first step less intimidating.

Saving money is a great first step. But if your money is just sitting in a savings account, it's actually losing value over time. Prices keep rising – a gallon of milk costs a lot more today than it did 20 years ago – and your savings aren't keeping pace.

That's where investing comes in.

If the word "investing" makes you think of Wall Street traders or people with a lot more money than you, you're not alone. Most people were never taught this in school. But investing isn't just for the wealthy. It's a tool anyone can use, and the earlier you start, the more powerful it becomes.

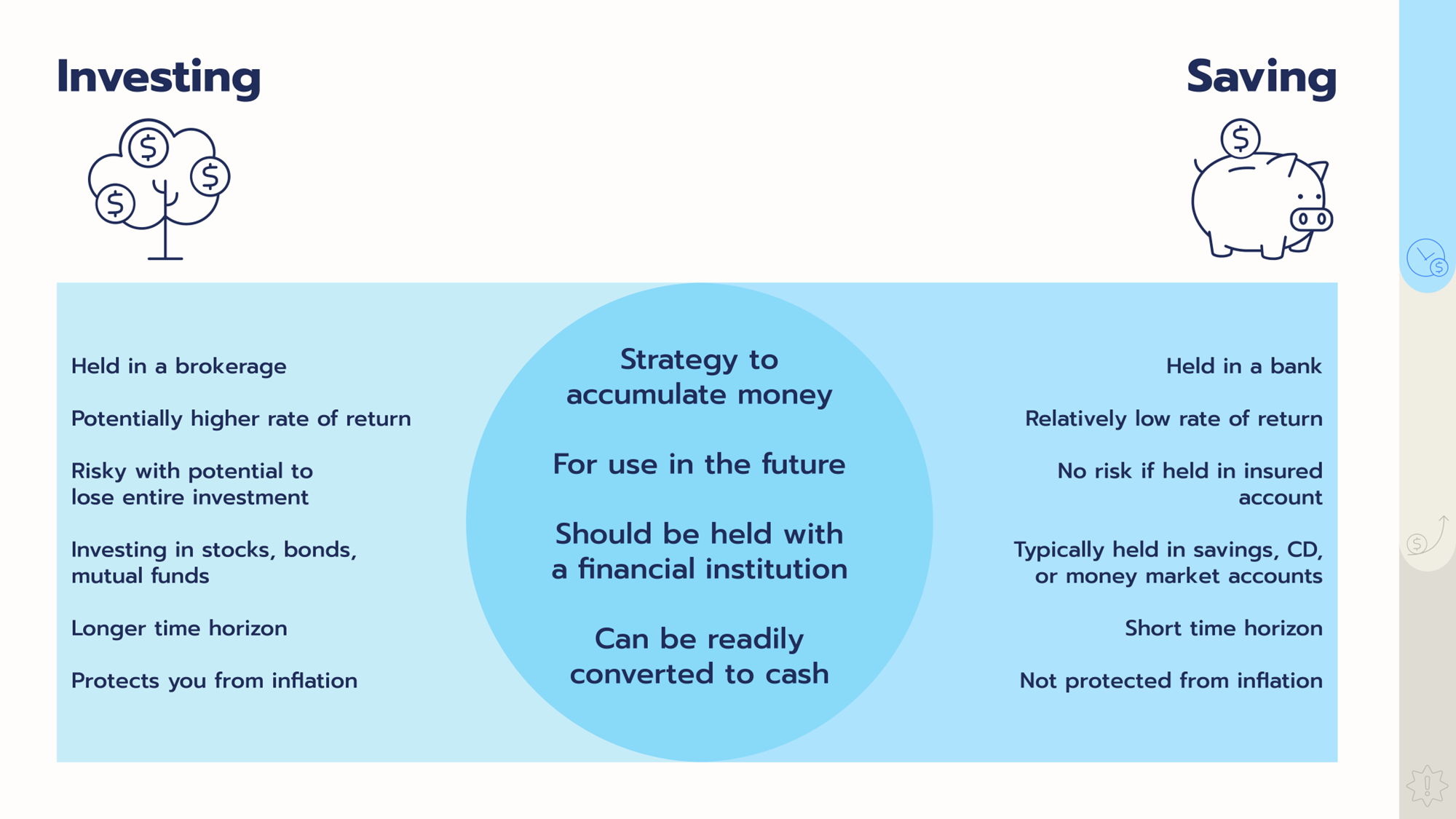

Saving vs. investing: what's the difference?

Both saving and investing are strategies to accumulate money for future use. But they work very differently. Below is a picture that can help visualize the similarities and differences.

* Financial Beginnings – Foundations Investing 1 Slide Deck

* Financial Beginnings – Foundations Investing 1 Slide Deck

Inflation is the gradual rise in prices over time and a savings account won't grow fast enough to keep up with it. Investing can.

Both saving and investing have a place in a healthy financial plan. Savings is for money you might need soon. Investing is for money you won't need for years.

H2 – The power of starting early

Time is the most powerful ingredient in investing. Below are two scenarios to visualize how investing at different life stages and amounts can make a difference.

* Financial Beginnings – Foundations Investing 1 Slide Deck

* Financial Beginnings – Foundations Investing 1 Slide Deck

Now, consider these two investors, Caden and Jaye. who each contribute $50 a month:¹

|

Caden |

Jaye |

|

|

Starts at |

Age 20 |

Age 30 |

|

Contributes for |

10 years |

30 years |

|

Contribution per month |

$50 |

$50 |

|

Total contributed |

$6,000 |

$18,000 |

|

Value at age 60 |

$204,873 |

$113,966 |

Jaye contributed three times as much over three times as many years. Caden still came out ahead by nearly $91,000, simply by starting earlier and letting time do the work.

The lesson isn't that Jaye did anything wrong. She still built something meaningful. The lesson is that starting earlier can be more powerful than contributing more and time is one of the most valuable tools in investing.

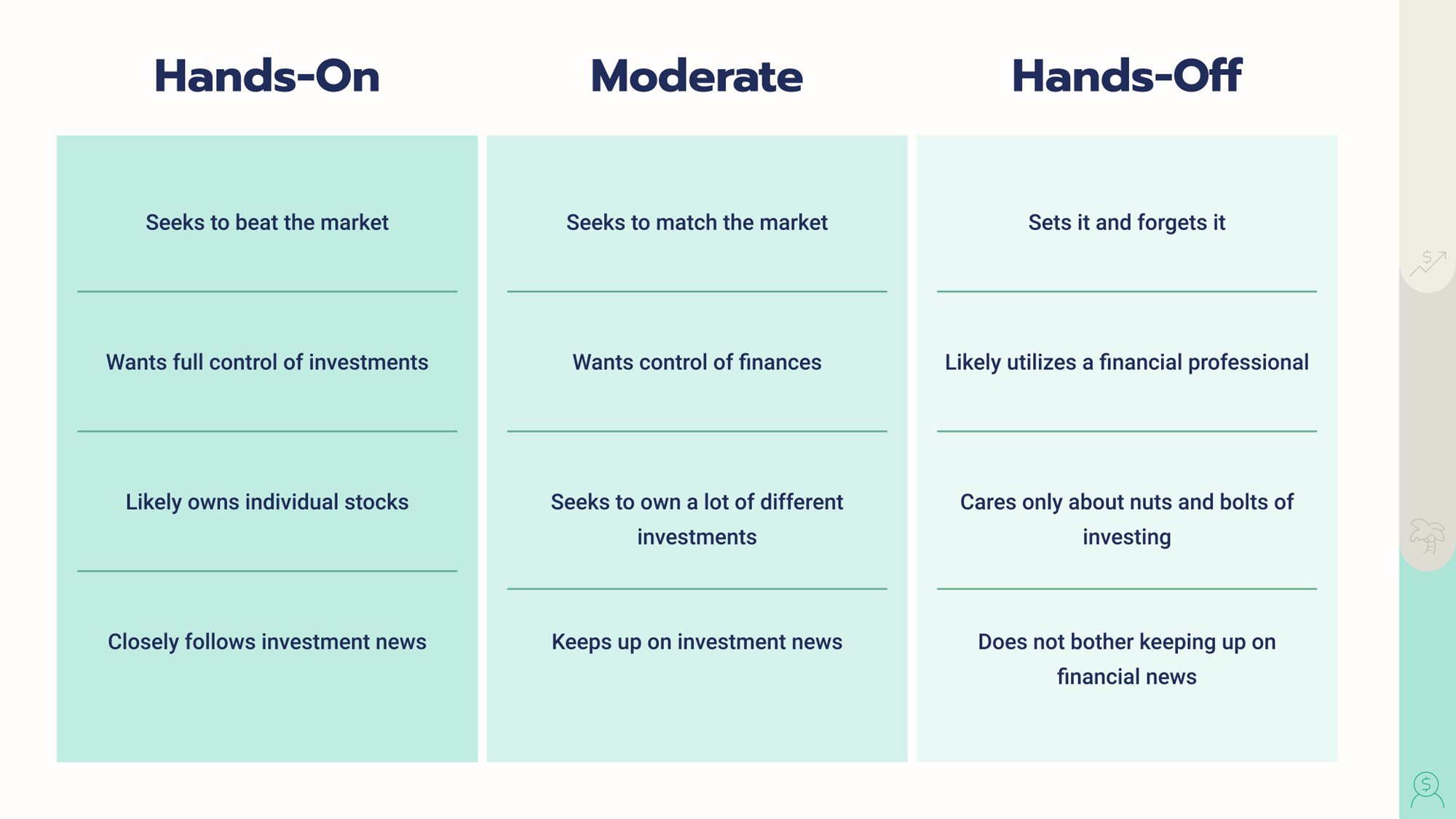

Investor type and risk profile

Before you choose any investment, it helps to know your investor type and risk profile.

Here is a tool to determine your investor type:

* Financial Beginnings – Foundations Investing 2 Slide Deck

* Financial Beginnings – Foundations Investing 2 Slide Deck

When it comes to risk profile, you can ask yourself these two questions:

|

What it means |

Ask yourself |

|

|

Time horizon |

How long before you'll need this money |

Am I investing for next year or the next decade? |

|

Risk tolerance |

How much uncertainty you can handle without panicking |

Could I sleep at night if my balance dropped 20%? |

The younger you are and the longer your time horizon, the more risk you can afford to take. As you get closer to needing the money, shifting toward more stable investments helps protect what you've built. Investor types and your tolerance to risk will vary over time.

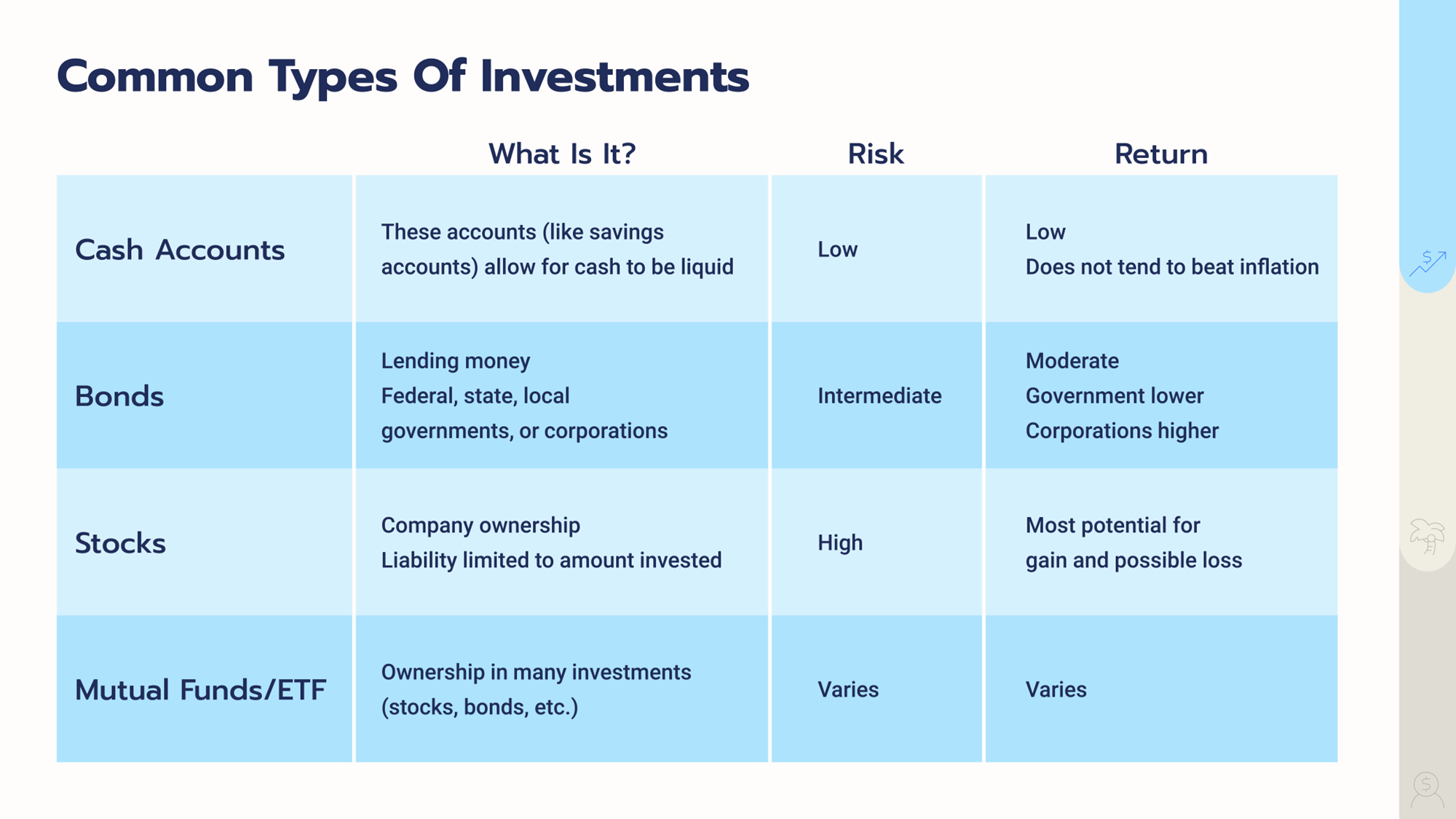

Common types of investments

It can be overwhelming to decide where to begin with so many different types of investments products!

Here are some of the common ones that you may have heard before.

* Financial Beginnings – Foundations Investing 2 Slide Deck

* Financial Beginnings – Foundations Investing 2 Slide DeckOne important concept across all of these: diversification. Spreading your money across different types of investments means one bad pick won't sink your whole portfolio. Think of it as not putting all your eggs in one basket. Mutual funds and ETFs all build diversification in automatically.

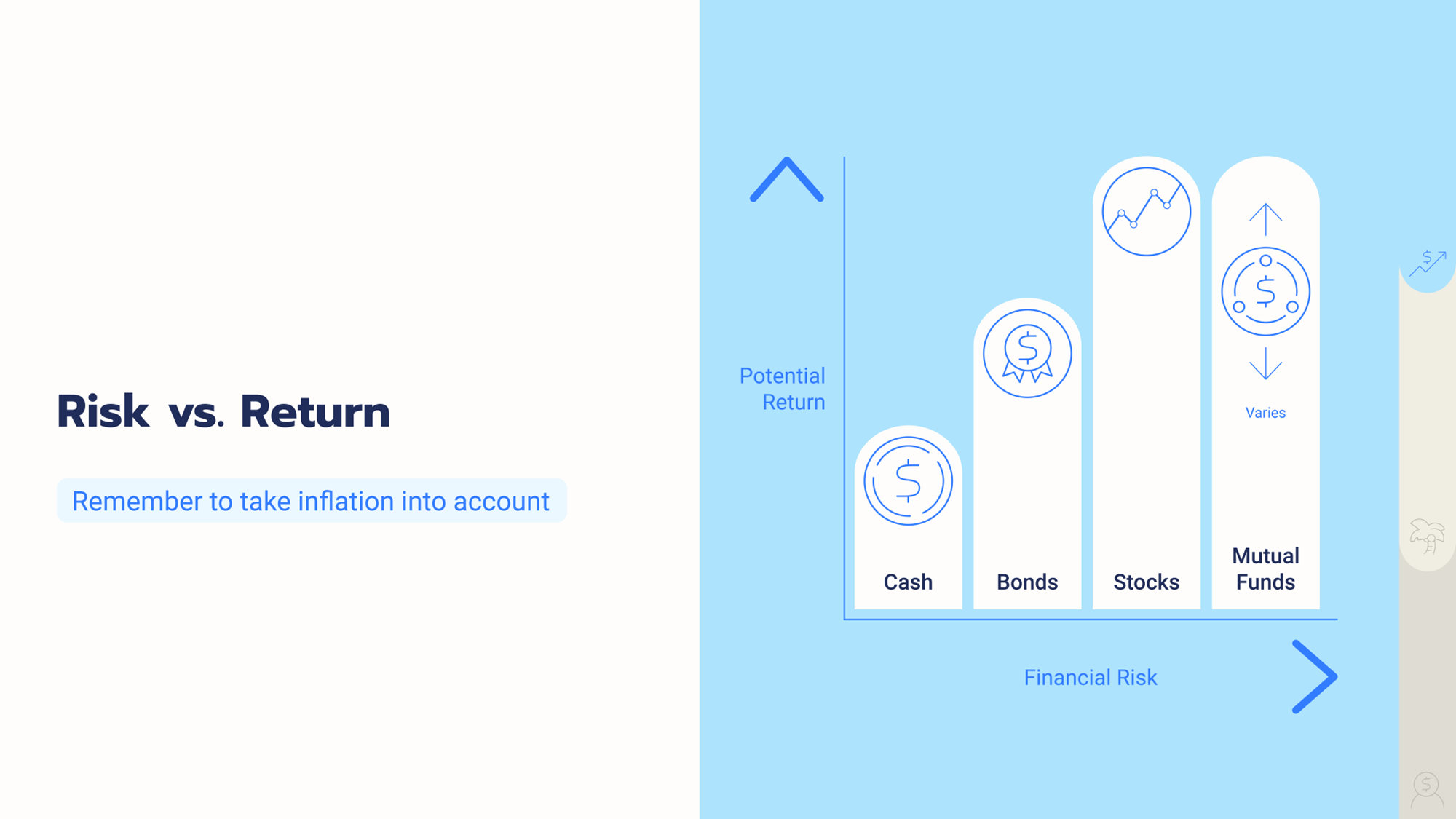

Risk vs. return

Every investment involves a tradeoff. Higher potential return means higher risk. Lower risk means lower potential reward.

* Financial Beginnings – Foundations Investing 2 Slide Deck

* Financial Beginnings – Foundations Investing 2 Slide Deck

If the idea of losing money keeps you on the sidelines, you're not alone. But history offers some perspective.

Even through recessions, market crashes, and global crises, the stock market has averaged around 10% growth per year over the long run.⁴

Bonds have averaged around 5%.²

A mutual fund that has historically averaged around 8–9% annually, offering a smoother ride without giving up too much growth.³

Neither extreme is right or wrong for everyone. It depends on your timeline and your goals.

Okay, So Where Do I Actually Start?

Once you know what you want to invest in, you need a place to hold those investments. Here's how the main account types compare.

|

401(k) / 403(b) |

Traditional IRA |

Roth IRA |

Brokerage Account |

|

|

Who opens it |

Employer |

You |

You |

You |

|

Tax treatment |

Pre-tax contributions, taxed on withdrawal |

Pre-tax contributions, taxed on withdrawal |

After-tax contributions, tax-free growth |

No tax advantages |

|

2026 Contribution limit |

$24,500/yr⁵ |

$7,500/yr⁵ |

$7,500/yr⁵ |

No limit |

|

Employer match |

Often yes |

No |

No |

No |

|

Early withdrawal |

Penalties apply |

Penalties apply |

Contributions only, no penalty |

Anytime, no penalty |

|

Best for |

Getting started, especially with a match |

Tax break now, pay later |

Tax-free growth, pay now |

Flexibility beyond retirement accounts |

Employer-Sponsored Retirement Accounts (401k and 403b) If your employer offers a match, start here. Contributions come out of your paycheck before taxes, and that employer match is free money.

Individual Retirement Accounts (IRAs) An IRA is a retirement account you open on your own. A Traditional IRA lowers your tax bill today. A Roth IRA lets your investments grow completely tax-free – often the smarter move for beginners earlier in their careers.⁵

Brokerage Account The most flexible option. No contribution limits, no withdrawal restrictions, and no minimum to get started. Best for goals beyond retirement.

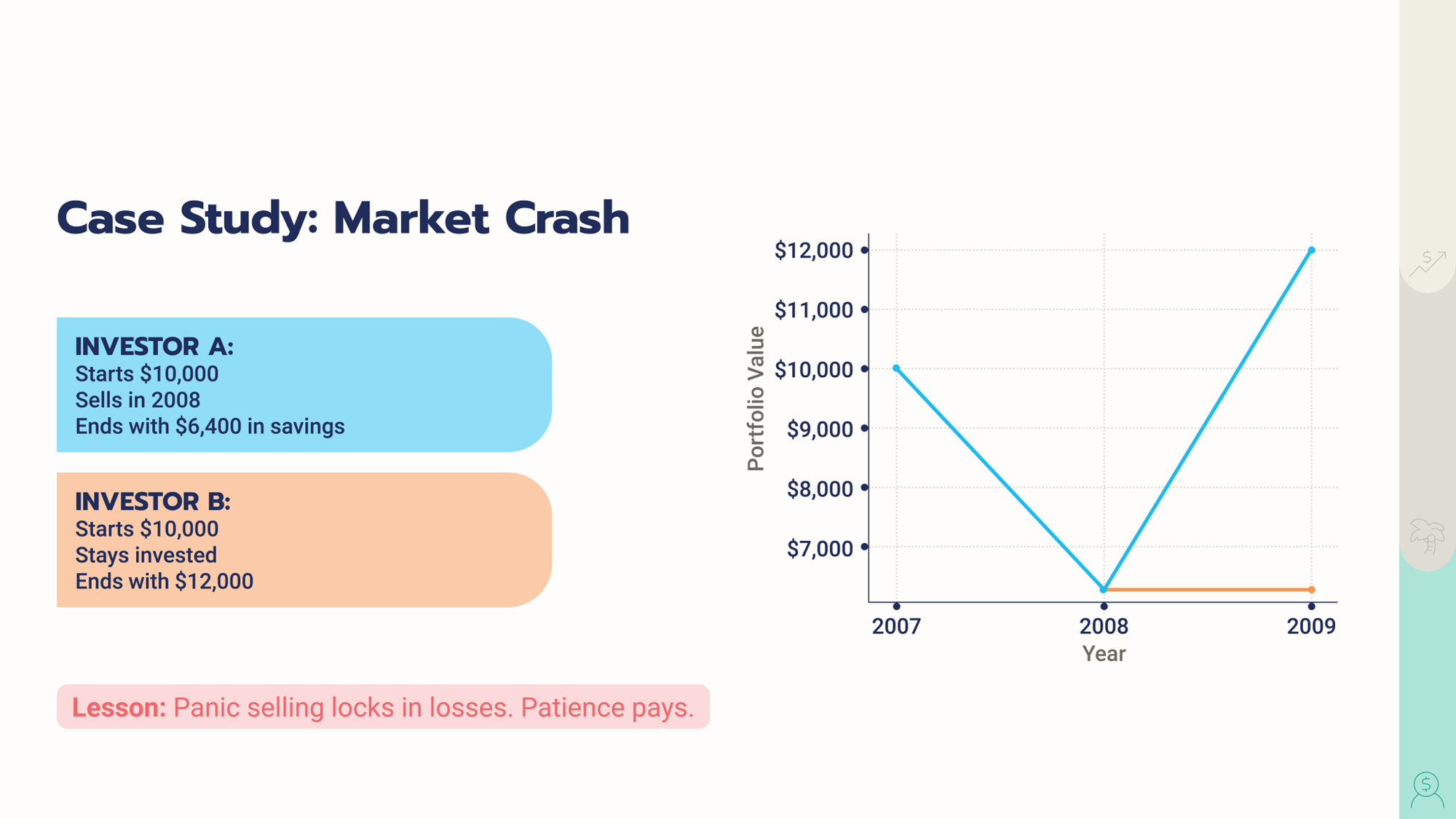

What happens when the market drops

At some point, it will. Markets go up and down – that's normal and expected.

The instinct when your balance drops is to pull your money out and wait for things to stabilize. But that instinct works against you. When you sell during a downturn, you lock in your losses. When the market recovers – and historically it always has – you miss the rebound.

Consider the example below. Investor A started with $10,000, panicked in 2008, sold everything, and ended with just $6,400. Investor B also started with $10,000 but stayed invested and grew their account to $12,000.

* Financial Beginnings – Foundations Investing 2 Slide Deck

* Financial Beginnings – Foundations Investing 2 Slide Deck

Staying invested, even during uncomfortable stretches, is one of the most important things you can do as a beginner investor. This is also why knowing your risk tolerance matters. If a market dip causes so much anxiety that you're likely to sell, your investments might be riskier than they should be for your timeline.

Your action plan

You don't need to figure it all out today. Pick the step that fits where you are right now.

- Open a high-yield savings account if you haven't already. It's a low-risk first step to earning more on money you're already setting aside.

- Check if your employer offers a 401(k) or 403(b) match. That's free money. Contribute at least enough to get the full match.

- Consider a Roth IRA. If you have earned income, a Roth IRA lets your investments grow completely tax-free.

- Look into a low-cost index fund. An S&P 500 index fund is where most financial educators recommend beginners start.

- Open a brokerage account for goals beyond retirement. Many platforms let you start with as little as $1.

- Start small and stay consistent. $25 a month beats $0 a month. The habit matters more than the amount.

Financial Beginnings is a national nonprofit dedicated to making money and finance easier to understand through practical, unbiased financial education.

Every step forward counts, no matter how small. Taking time to learn about your finances is always a step in the right direction. Want to keep building your financial knowledge? The Financial Beginnings Online eLearning platform offers free, self-paced courses on essential personal finance topics — available anytime, anywhere. Browse our growing library of lessons designed to help you take control of your financial future.

¹ Projections assume a 10% annual rate of return, compounded monthly. These figures are for illustrative purposes only and are not a guarantee of future results.

² Information from Morningstar's historical bond return data via Retirement Researcher's "Historical Market Returns – Part Two" as of September 6, 2024: retirementresearcher.com/historical-market-returns-part-two/

³ Information from Barbara Friedberg Personal Finance's "Historical Stock and Bond Returns" as of January 13, 2026: barbarafriedbergpersonalfinance.com/historical-stock-and-bond-returns/

⁴ Information from Dimensional Fund Advisors' "The Uncommon Average" as of 2024: dimensional.com/us-en/insights/the-uncommon-average

⁵ Information from the Internal Revenue Service's "401(k) limit increases to $24,500 for 2026, IRA limit increases to $7,500" as of November 13, 2025: irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500